.png)

Snapshot of key economic indicators | April 2025

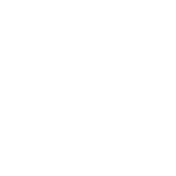

Impact of ‘discounted tariffs’ on Indian industry sectors

On April 2, 2025, a day proclaimed by US President Donald Trump as ‘Liberation Day’, a sweeping set of reciprocal tariffs was rolled out to target countries with sustained trade surpluses. While the move affects global trade flows, its impact on India is nuanced – offering both risks and selective opportunities depending on the sector and competitive dynamics.

Timeline of key events

India – US trade

USA is India’s largest export destination, accounting for 17.7% of India’s overall exports in FY 2023-24.

|

Year |

India’s total export (USD billion) |

India’s export to US (USD billion) |

Percentage |

|

2022-23 |

451.07 |

78.54 |

17.4 |

|

2023-24 |

437.07 |

77.51 |

17.7 |

|

Apr’24 – Jan’25 |

358.63 |

68.45 |

19 |

While the US tariffs of 2025 will affect various Indian industry sectors, the country’s competitive positioning in some areas can help mitigate the negative impact, especially when compared to competitors like China, Vietnam, and the European Union (EU).

Sectoral impact on Indian industry

DPIIT’s Press Note 2 (2025)

The Department for Promotion of Industry and Internal Trade (DPIIT) has recently released its Press Note 2 (2025) (Press Note) clarifying that Indian companies engaged in sectors or activities prohibited for Foreign Direct Investment (FDI) are authorised to issue bonus shares to their pre-existing non-resident shareholder(s) provided that their shareholding pattern does not change in accordance with the issuance of bonus shares.

While companies operating in sectors prohibited under the FDI policy, such as tobacco, lottery, gambling, chit funds, and atomic energy, are barred from receiving new foreign investment, they often have existing non-resident shareholders whose investments were made prior to the imposition of sectoral FDI restrictions. The existence of such ‘grandfathered’ investments (permissible under the old law) did not automatically clarify the permissibility of bonus issuances, which, although non-cash in nature, could impact shareholding patterns. Such companies, with significant foreign shareholding, have adopted a cautious approach by seeking prior Reserve Bank of India (RBI) approval.

The Press Note explicitly amends Paragraph 1 of Annexure 3 of the FDI Policy, stating that Indian companies in FDI-prohibited sectors are now allowed to issue bonus shares to their existing non-resident shareholders, provided there is no change in the relative shareholding pattern post-issuance. This means that the proportional ownership of non-resident shareholders must remain the same, effectively preventing any indirect increase in foreign control and maintaining the integrity of FDI restrictions. This permission is further subject to compliance with applicable laws such as the Companies Act, 2013

The Press Note will come into force upon issuance of the relevant notification under the Foreign Exchange Management 1999, (FEMA), with corresponding amendments expected shortly in the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019.

In addition to bringing clarity on the ability of companies in sensitive sectors to issue bonus shares to carry out legitimate corporate actions, including bonus issuances, without breaching FDI norms, the Press Note removes the existing requirement for prior RBI approval, thereby reducing bureaucratic delays and simplifying the compliance process. This reform also boosts investor confidence, enhances regulatory clarity, and ensures that compliant foreign shareholders are not unfairly excluded from the benefits of such actions. Despite this positive development, the issue of whether bonus issues that result in shifts in voting power between resident and non-resident shareholders, due to factors like non-participation or rounding off, would inevitably come under regulatory scrutiny.

Profit-sharing agreement involving reciprocal obligations is not financial borrowing

In a recent decision, the National Company Law Tribunal, New Delhi (NCLT) held that a profit-sharing agreement involving reciprocal obligations in the nature of speculative investment is not a financial debt and cannot be used to initiate Corporate Insolvency Resolution Process (CIRP).1

Krrish Realtech Pvt Ltd (Corporate Debtor/CD) entered into a Memorandum of Understanding (MoU) with MK Jain and his family (Applicants) whereby the Applicants were to advance INR 15 crore as investment (Investment) in consideration of which the CD would purchase allot certain plots belonging to Kelvin Buildcon Pvt Ltd (Kelvin Plots) and allot them to the Applicants by a specified ‘cut-off date’. Clause 5 placed a reciprocal obligation on the Applicants requiring them to sell the Kelvin Plots in the market on the following conditions:

The CD could not allot the Kelvin Plots by the cut-off dates resulting in breach of the MoU. The Applicants initiated arbitration and secured an interim award in their favour, on the basis of which the Applicants sought initiation of CIRP against the CD under Section 7 of the Insolvency and Bankruptcy Code, 2016 (Code) contending that the Investment was in the nature of a financial borrowing.

The NCLT dismissed the CIRP application and held that since the MoU contained reciprocal rights and obligations and the nature of the transaction was to share the profits, the Applicants would receive a residual gain upon the fulfilment of the Agreement. As such, the transaction was in the nature of speculative investment, which did not qualify as a ‘financial debt’ under the Code.

The decision underscores the importance of distinguishing between genuine financial borrowings and speculative investments structured as commercial arrangements. Parties advancing funds with the expectation of profit-sharing or contingent returns based on future events must be cautious as such arrangements may fall outside the ambit of ‘financial debt’ under the Code. Investors should ensure that lending arrangements reflect the characteristics of a loan (such as fixed returns, clear repayment terms, and consideration for time value of money) to avoid adverse outcomes in enforcement.

Draft amendments to the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016

In a bid to simplify and expedite corporate restructuring, the Ministry of Corporate Affairs (MCA) has proposed amendments to the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 (Rules). These changes aim to significantly expand the scope of fast-track mergers under Section 233 of the Companies Act, 2013. The proposed amendments, originally announced as part of the Union Budget 2025-26, are now open for stakeholder comments till May 5, 2025.

Fast-track mergers were introduced in 2016 to facilitate quicker corporate restructurings between certain classes of companies without requiring approval of the National Company Law Tribunal (NCLT). Currently, this route is limited to:

The proposed amendments significantly widen the scope of entities eligible for fast-track mergers by including the following new categories:

By removing the requirement for approval by the NCLT, the most significant benefit of the proposed amendments is the reduced compliance burden and approval timelines, allowing companies to restructure without having to navigate lengthy and often complex litigation. The reform is particularly supportive of start-ups and MSMEs, thus encouraging innovation and growth. Additionally, by permitting mergers between fellow subsidiaries and expanding the scope of permissible holding-subsidiary combinations, the amendments promote group synergies and enable companies to undertake internal restructuring more efficiently. Introducing objective thresholds (such as debt limits and non-default status) has enabled more businesses to leverage simplified routes without compromising creditor protection or investor confidence. The proposed reform is a progressive step aligned with India's larger goal of enhancing its ease of doing business.

SEBI’s consultation paper on proposed amendments to the SBEBSE Regulations, 2021

In a significant move aimed at resolving longstanding ambiguity, the Securities and Exchange Board of India (SEBI) has proposed an amendment to the SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021 (SBEBSE Regulations) to clarify that Employee Stock Option Plans (ESOPs), Stock Appreciation Rights (SARs), or similar benefits granted to founders before they are identified as ‘promoters’ in a Draft Red Herring Prospectus (DRHP) will remain valid and exercisable post-listing. To prevent misuse, this exemption will apply only to grants made at least 1 year prior to the company’s IPO decision.

Existing framework

Since many startup founders initially receive ESOPs as part of their compensation and incentives, they often become classified as promoters when preparing for an IPO. The current framework does not explicitly clarify whether a founder who has been granted ESOPs before the DRHP filing can exercise them upon being reclassified as a promoter at the time of listing, leading to uncertainty and concerns among founders regarding their ESOPs benefits.

Clarification by SEBI

To address this ambiguity, SEBI has proposed to add an Explanation to Regulation 9(6) of the SBEBSE Regulations, and clarify the following:

Benefits of the proposed amendment

The proposed clarification is a progressive step towards fostering a more startup-friendly regulatory environment and will significantly impact how startups approach IPOs in India. It reinforces SEBI’s commitment to balancing regulatory oversight with flexibility for high-growth companies, making India’s capital markets more attractive for emerging businesses.

SEBI (Issue of Capital and Disclosure Requirements) Amendment Regulations, 2025

The Securities and Exchange Board of India (SEBI) has approved amendments to the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (ICDR Regulations), formally incorporating Stock Appreciation Rights (SARs) within the regulatory framework. The amendments, effective from March 8, 2025, will significantly impact capital raising, compliance obligations, and regulatory oversight.

SARs allow employees to benefit from the increase in a company’s stock price without requiring them to purchase shares upfront. Unlike Employee Stock Option Plans (ESOPs), which mandate employees to pay an exercise price to acquire shares, SARs grant them the right to receive the equivalent of stock price appreciation in cash or equity upon vesting, offering a gain without the financial risk of owning stock. Many companies prefer stock-based SAR settlements as a means of conserving cash reserves.

The amendment formally recognises SARs as a valid equity-linked instrument for regulatory purposes. This marks a significant shift, particularly in the context of Initial Public Offerings (IPOs) and ESOPs, where SARs were previously unregulated or ambiguously treated, aligning SAR treatment with ESOPs.

This recognition entails the following regulatory changes:

By provide regulatory certainty, the amendments are expected to make SARs a more integral part of corporate compensation strategies in India. While the added regulatory clarity is likely to encourage more companies to use SARs to attract and retain talent, companies must exercise caution against its overuse and carefully navigate additional compliance requirements in the usage, valuation, and disclosure of SARs.

The amendment enhances investor protection, corporate accountability, and disclosure standards. However, as its adoption grows, further refinements regarding SAR-based equity issuances may be necessary for standardising valuation methods, improving disclosure norms, and strengthening investor protection measures.

No automatic right to interest under IBC

In a recent decision, the National Company Law Appellate Tribunal, New Delhi (NCLAT) held that the interest component mentioned in an unsigned invoice cannot be incorporated in the claim amount.2

Jai Narayan Fabtech Pvt Ltd (Operational Creditor/OC) supplied polyester staple fibre to Cheema Spintex Ltd (Corporate Debtor/CD) on various occasions along with invoices. The CD defaulted in making payments and the OC initiated CIRP on a principal claim of INR 74 lakh along with interest on account of delayed payment at 12% per annum (as per the terms of the invoices), amounting to INR 85 lakh, totalling to INR 1.59 crore.

The NCLAT noted that the invoice (which mentioned the interest component) was not signed by the CD and was therefore a unilateral document. As such, interest cannot be recovered on the basis of the unsigned invoice. As the interest component could not be claimed, the claimed amount fell below the INR 1 crore threshold as per Section 4 of the Insolvency and Bankruptcy Code, 2016 (Code).

This decision highlights the critical importance of evidencing mutual agreement on key commercial terms, particularly interest on delayed payments, in insolvency proceedings. Creditors cannot rely on unilateral documents, such as unsigned invoices, to substantiate interest claims. Operational creditors must ensure that terms relating to interest are expressly agreed upon in writing and acknowledged by the CD, whether through signed contracts, purchase orders, or confirmed invoices. In cases involving multiple or recurring shipments, suppliers would be well-advised to seek a signed acknowledgment of each invoice, especially where interest or specific payment terms are stipulated, before proceeding with subsequent deliveries. This not only strengthens the evidentiary value of the claim but also safeguards enforceability under the Code.

Similarly, in a separate decision, the National Company Law Tribunal, Mumbai (NCLT) has clarified that the Code does not create any automatic right to claim interest on the principal claim (default).3 The language of Regulation 16A(7) of the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations), ‘The voting share of a creditor in a class shall be in proportion to the financial debt which includes an interest at the rate of eight per cent per annum’ merely provides for the calculation of the voting share of a creditor in a class and does not create an automatic entitlement with respect to interest that must be included in a resolution plan.

IBBI (Insolvency Resolution Process for Corporate Persons) (Second Amendment) Regulations, 2025

The Insolvency and Bankruptcy Board of India (IBBI) has amended the IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations) introducing revisions to Form H of Schedule I required to be submitted by the Resolution Professional (RP) along with the resolution plan approved by the Committee of Creditors (CoC) to the Adjudicating Authority.

The updated Form H requires details of the following information:

Notification by the Ministry of Micro, Small and Medium Enterprises

The Ministry of Micro, Small and Medium Enterprises has recently issued a notification in supersession of its earlier notification dated June 26, 2020, re-classifying Micro, Small, and Medium Enterprises (MSMEs) by revising the limits for investment in plant, machinery, and equipment and for turnover as follows:

|

Enterprise |

Current |

Revised |

|

Micro Enterprise |

Investment limit: INR 1 crore Turnover limit: INR 5 crore |

Investment limit: INR 2.5 crore Turnover limit: INR 10 crore |

|

Small Enterprise |

Investment limit: INR 10 crore Turnover limit: INR 50 crore |

Investment limit: INR 25 crore Turnover limit: INR 100 crore |

|

Medium Enterprise |

Investment limit: INR 50 crore Turnover limit: INR 250 crore |

Investment limit: INR 125 crore Turnover limit: INR 500 crore |

The re-classification of MSMEs is likely to lead to the following benefits:

The reclassification is accompanied by an enhancement of credit guarantee, doubling the credit guarantee cover from INR 5 crore to INR 10 crore. This is expected to unlock INR 1.5 lakh crore in additional credit over 5 years.

Additionally, in line with the mandatory 45-day payment period (for companies procuring goods/services from Micro and Small Enterprises) specified under Section 15 of the Micro, Small and Medium Enterprises Development Act, 2006, any company exceeding such statutory period would be required to submit a half-yearly return to the Ministry of Corporate Affairs (MCA) stating the amount of payment due and the reasons of the delay.

The details, which were earlier required to be filed in Form MSME – 1 with the Registrar of Companies (RoC), are now also to be filed with the MCA by October 31 (for the period of April to September) and by April 31 (for the period of October to March). Failure to do so would entail penalties of upto INR 3 lakh as per Section 405(4) of the Companies Act, 2013.

Eligibility criteria for fast-track route removed

The Securities and Exchange Board of India (SEBI) has significantly simplified the regulatory regime governing rights issue by a listed company through amendments to the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (ICDR Regulations). These changes, effective from April 7, 2025, aim to expedite rights issue, reduce compliance costs, streamline disclosures, enhance investor protection, and introduce flexible participation models, in line with contemporary market dynamics.

A rights issue allows existing shareholders to subscribe to additional shares in proportion to their existing holdings, typically at a discount. Governed under Section 62(1) of the Companies Act, 2013 and Regulation 2(1)(xx) of the ICDR Regulations, this mechanism enables companies to raise capital while offering existing investors the opportunity to maintain their shareholding percentage.

Key changes in the framework for rights issue are as follows:

SEBI’s reforms address a long-standing criticism regarding the slow and cumbersome framework of rights issue compared to alternative fundraising modes. As per SEBI’s 2024 annual report, rights issues raised INR 6,751 crore and INR 15,110 crore in FY 2022-23 and FY 2023-24, respectively, significantly less than the INR 83,832 crore and INR 45,115 crore raised via preferential allotments in the same periods. This progressive regulatory shift is expected to make rights issue a more attractive and viable capital-raising tool for listed companies. For investors, the changes offer enhanced transparency, faster execution, and expanded participation options, marking a robust step toward a modern, efficient, and inclusive securities market.

Monetary policy changed from ‘accommodative’ to ‘neutral’

The Reserve Bank of India’s (RBI) Monetary Policy Committee has cut the repo rate by 25 basis points for the second consecutive time, lowering it from 6.25% to 6.00%. This policy change from ‘accommodative’ to ‘neutral’ comes in the wake of the United States tariffs, which threaten RBI’s Gross Domestic Product (GDP) growth estimate of 6.7%.

This reduction in the repo rate is expected to provide relief to borrowers, particularly those with floating-rate home loans, as banks and financial institutions begin to pass on the benefits through lower interest rates. In addition to reducing Estimated Monthly Instalments (EMIs), the rate cut could spur greater credit demand, encourage consumer spending, and support investment activity.

Foot note:

1MK Jain v. Krrish Realtech Pvt Ltd, Company Petition (IB) No. 348 of 2024

2 Jai Narayan Fabtech Pvt Ltd v. Cheema Spintex Ltd, Company Appeal (AT) (Ins) No. 1515 of 2023

3Klassic Wheels Ltd v. Amit Vijay Karia, Company Petition (IB) No. 715 of 2021

Banking & Finance

Banking & Finance

Capital Markets & Securities Law

Capital Markets & Securities Law

Corporate & Commercial

Corporate & Commercial

Insolvency & Restructuring

Insolvency & Restructuring